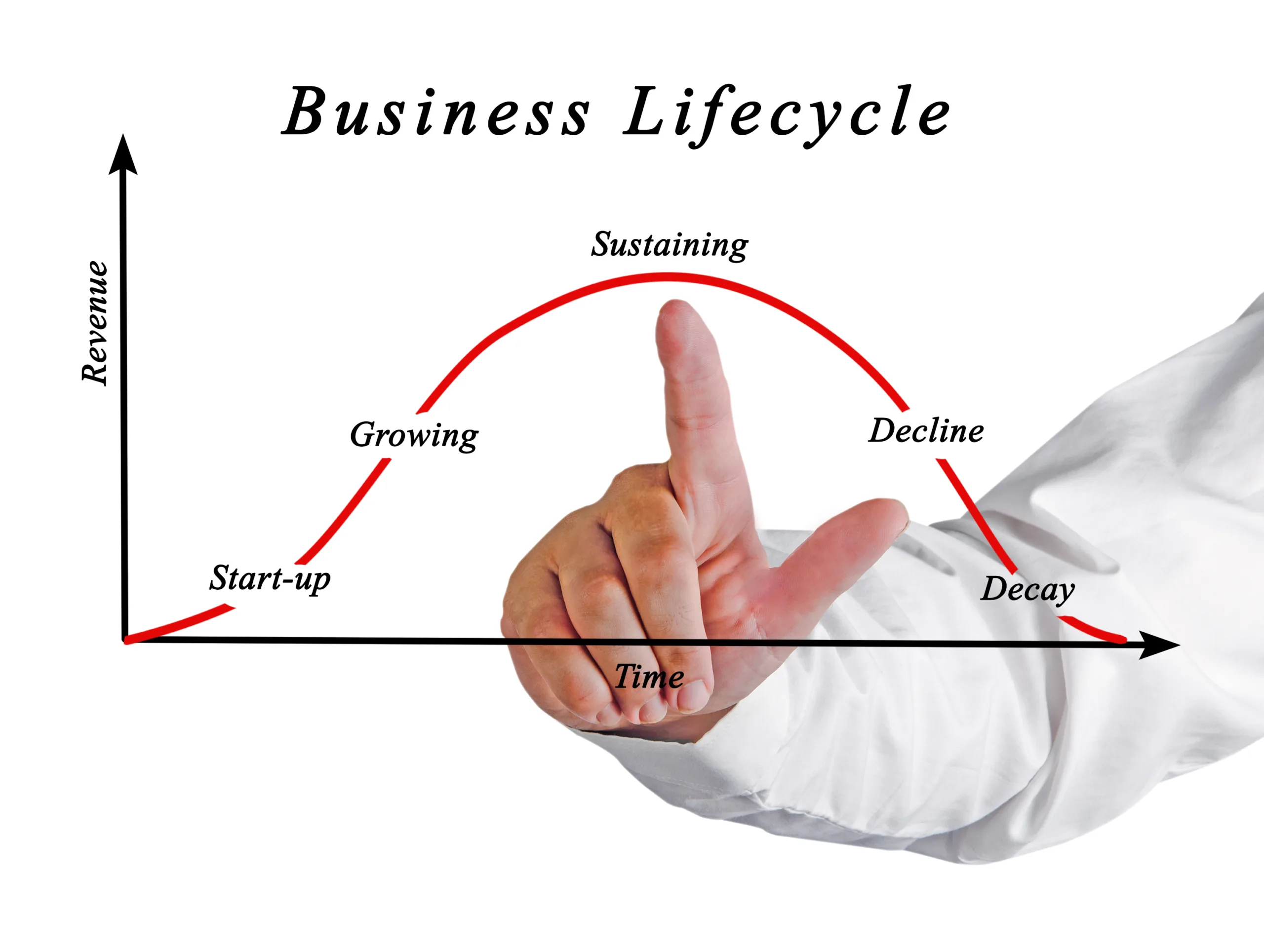

The lifecycle of a business is a series of stages that each company inevitably goes through, from the spark of an idea to the maturity and eventual decision on the future direction. Understanding these stages is crucial for effective management and strategic planning and ensuring your business’s longevity and success.

This article will equip business owners with practical advice and insights on managing through the different stages of the business lifecycle. Whether you’re in the throes of launching your startup, looking to scale, or facing the challenges of renewal or decline, this guide offers strategies to navigate these transitions smoothly. By understanding what each stage entails and preparing for the challenges and opportunities they present, you can make informed decisions that align with your business goals and market demands.

Stage 1: Ideation and Conception

At the heart of every successful business lies a compelling idea. Everything begins in the ideation and conception stage, from a spark of inspiration to formulating a business concept to fill a market gap or improve existing products or services. This foundational stage is crucial, as it sets the direction for your business journey. Here are key steps and considerations for effectively navigating the ideation and conception phase.

Defining the Business Idea

- Market Research: Start with thorough market research to understand the needs of your target audience and identify gaps in the current market. This can involve analyzing competitors, understanding industry trends, and identifying potential customer pain points.

- Innovation: Consider how your business can offer something unique or improve upon existing solutions. Innovation doesn’t necessarily mean inventing something entirely new; it can also mean delivering existing products or services more efficiently, cost-effectively, or user-friendly.

- Feasibility Study: Evaluate the feasibility of your idea by considering factors like potential market size, revenue models, and startup costs. This will help you determine if your idea has the potential to turn into a viable business.

Crafting a Solid Business Plan

- Structure and Objectives: Outline your business’s structure, goals, and objectives. A well-crafted business plan serves as a roadmap for your business, detailing how you plan to achieve your goals.

- Financial Planning: Include detailed financial projections and plans, covering startup costs, funding requirements, revenue forecasts, and break-even analysis. This part of your business plan is critical for securing funding and managing your finances effectively.

- Market Strategy: Develop a clear market entry strategy that outlines how you will reach your target customers, including marketing channels, pricing strategies, and sales plans.

Initial Funding and Resource Allocation

- Identifying Funding Sources: Explore various funding options, including personal savings, loans, angel investors, venture capital, or crowdfunding. Choose the best mix of funding sources that align with your business needs and growth plans.

- Resource Allocation: Plan how you will allocate your initial funds across various aspects of your business, such as product development, marketing, and operations. Efficient resource allocation is critical to stretching your startup budget and achieving early milestones.

The ideation and conception stage is about laying a solid foundation for your business. It requires creativity, strategic planning, and a keen understanding of the market you intend to enter. By thoroughly researching your idea, crafting a detailed business plan, and securing the necessary funding, you set the stage for a successful launch and future growth. Remember, the decisions and plans you make during this initial stage will shape the direction and success of your business for years to come.

Stage 2: Startup and Establishment

Transitioning from an idea to a functioning business is a significant leap. Your planning meets reality in the startup and establishment stage, and your concept becomes tangible. This phase involves navigating legal requirements, building a team, launching your product or service, and establishing operational workflows. Here’s how to manage these crucial steps effectively.

Legalities and Paperwork

- Choosing the Right Business Structure: Determine the most appropriate legal structure for your business, such as a sole proprietorship, partnership, limited liability company (LLC), or corporation. Each has its implications for taxes, liability, and business operations.

- Registering Your Business: Complete the necessary registration with local, state, and federal authorities. This might include obtaining a tax identification number, business licenses, and permits.

- Protecting Your Business: Consider insurance policies to protect your business and its assets. Also, safeguard any intellectual property through copyrights, trademarks, or patents as applicable.

Building a Team

- Hiring Strategies: Identify critical roles to fill and begin the hiring process. Look for individuals with the necessary skills, share your vision, and fit the company culture.

- Developing a Supportive Culture: Create an environment encouraging innovation, collaboration, and open communication. A strong team dynamic will be essential as your business grows and faces new challenges.

Market Entry

- Launching Your Product or Service: To generate buzz and attract your target audience, plan a launch. This might involve a soft launch to gather initial feedback or a full-scale launch campaign.

- Initial Marketing Strategies: Develop marketing strategies that align with your budget and target market. Utilize a mix of digital marketing, content marketing, social media, and traditional advertising to reach your audience.

- Customer Feedback: Pay close attention to customer feedback and be willing to adjust your offerings. Early adopters can provide invaluable insights that help refine your product or service.

Setting Up Operations

- Operational Workflows: Establish efficient operational workflows to manage day-to-day activities. This includes logistics, inventory management, customer service, and financial management systems.

- Technology and Tools: Leverage technology to streamline operations, improve productivity, and enhance customer experiences. Consider tools for project management, customer relationship management (CRM), and financial tracking.

The startup and establishment stage is both exhilarating and challenging. It requires a focus on legal compliance, team building, market entry, and operational efficiency. By carefully navigating these steps, you can establish a solid foundation for your business, setting the stage for future growth and success. Flexibility and adaptability are essential during this stage as you learn from experiences and continuously refine your approach based on market feedback and operational insights.

Stage 3: Growth and Expansion

Once your business has navigated the startup phase and established its presence in the market, the next challenge is to grow and expand. This stage is characterized by increasing sales, expanding the customer base, and possibly entering new markets or launching new products. Growth is exciting but requires careful planning and management to ensure sustainable success. Here’s how to effectively manage the development and expansion of your business.

Scaling Operations

- Efficiency and Automation: As your business grows, finding ways to operate more efficiently becomes crucial. Look into automating repetitive tasks and streamlining processes to handle increased demand without sacrificing quality or customer satisfaction.

- Capacity Planning: Assess your current capacity and identify areas that need scaling, such as production, staffing, and customer service. Planning for increased capacity ensures you can meet growing demand without overextending your resources.

Advanced Marketing Strategies

- Expanding Reach: With a solid customer base established, explore new marketing channels and strategies to reach a wider audience. This could include partnerships, influencer marketing, or expanding into new geographic markets.

- Customer Retention: Focus on retaining existing customers even when seeking new ones. Implement loyalty programs, personalized marketing, and exceptional customer service to engage and satisfy your current customers.

Financial Management

- Managing Cash Flow: Growth can often strain cash flow, so careful management is needed. Monitor your cash flow closely, plan for future expenses, and keep reserves for unexpected costs.

- Reinvestment: Decide how to reinvest profits wisely to support further growth. This could mean expanding your product line, investing in marketing, or upgrading equipment and technology.

- Seeking Additional Funding: You may need additional funding depending on your growth plans. Consider options like bank loans, venture capital, or equity financing to support your expansion efforts.

Strategic Partnerships and Alliances

- Building Relationships: Strategic partnerships with other businesses can open up new growth opportunities. Look for alliances that complement your business and offer mutual benefits.

- Entering New Markets: Partnerships can also be a valuable strategy for entering new markets, providing local insights and access to established customer bases.

The growth and expansion stage is a pivotal time for your business. It offers the opportunity to solidify your presence in the market, diversify your offerings, and build a stronger brand. However, it also comes with challenges, such as managing increased operational demands, ensuring financial stability, and maintaining the quality and integrity of your products or services. By focusing on efficiency, marketing, financial management, and strategic partnerships, you can navigate this stage successfully and set the stage for continued success and further expansion.

Stage 4: Maturity and Possible Saturation

Reaching the maturity stage is a significant achievement for any business, indicating stability, a loyal customer base, and a well-established position in the market. However, this stage brings challenges, such as increased competition, market saturation, and the need for continuous innovation to maintain growth. Here’s how to manage your business effectively during the maturity stage and address the potential for market saturation.

Maintaining Competitiveness

- Innovation: Continuous innovation is critical to staying relevant in a mature market. This could involve improving existing products or services, adopting new technologies, or enhancing customer experiences.

- Market Analysis: Regularly analyze the market and your competitors. Understanding shifts in customer preferences and competitive dynamics can help you adapt your strategies to remain competitive.

Understanding Evolving Customer Needs

- Customer Engagement: Maintain close engagement with your customers to understand their evolving needs. Use feedback mechanisms like surveys and social media interactions to gather insights.

- Adaptation: Be prepared to adapt your offerings based on customer feedback and market trends. This could mean diversifying your product line, offering customization options, or enhancing service levels.

Diversification

- Exploring New Markets: To avoid saturation and continue growing, consider exploring new markets. This could involve geographic expansion or targeting new customer segments.

- Product Line Expansion: Diversifying your product or service offerings can also help tap into new revenue streams and reduce dependence on your current market.

Efficiency and Cost Control

- Operational Efficiency: Review your operations for inefficiencies and identify areas where costs can be reduced without compromising quality. Streamlining operations can help improve margins and profitability.

- Cost Control: Implement strict measures to ensure your business remains financially healthy. This includes careful budgeting, reducing unnecessary expenses, and optimizing resource use.

In the maturity stage, you must balance what has made your business successful with innovating to stay ahead of the curve. While the risk of market saturation is real, it also presents an opportunity for your business to evolve and find new ways to grow. By focusing on innovation, customer engagement, diversification, and operational efficiency, you can navigate the challenges of this stage and set your business up for sustained success.

In some cases, despite best efforts, businesses may begin to see signs of decline. Recognizing these signs early and preparing for potential renewal strategies or considering graceful exit options is crucial. The following section will explore how to handle the renewal or decline phase, ensuring that your business remains proactive in its approach to the future.

Stage 5: Renewal or Decline

As businesses navigate the maturity stage, they may encounter signs of renewal or decline. This critical juncture requires astute leadership to either rejuvenate the business or manage its decline with dignity. Understanding your business’s trajectory and how to pivot or prepare for an exit is essential for long-term sustainability. Here’s how to approach both scenarios.

Recognizing Signs of Each Trajectory

- Renewal Indicators: Renewal may be signaled by opportunities for innovation, new market trends favoring your offerings, or emerging technologies that can revitalize your products or services.

- Decline Indicators: Signs of decline include consistently decreasing sales, diminishing market share, or increased competition that your business cannot match.

Renewal Strategies

- Rebranding: Sometimes, a fresh brand image or a repositioned message can reinvigorate interest in your offerings.

- Market Repositioning: Identifying and targeting new market segments or niches not well-served by your competitors can breathe new life into your business.

- Pivoting: This involves fundamentally changing a part of your business model to adapt to market changes or leverage new opportunities. It could affect your product lineup, target market, or business model.

Exit Strategies for Decline

- Succession Planning: If you’re considering stepping down, having a succession plan ensures your business continues under new leadership.

- Selling the Business: Finding a buyer can be a strategic move to ensure the business’s legacy while providing you with an exit.

- Liquidation: In cases where revival isn’t feasible, a structured approach to liquidating assets ensures that creditors and investors are fairly compensated.

Emotional and Financial Preparedness

- Emotional Resilience: Both renewal and exit strategies require emotional resilience from the business owner. Accepting change, facing potential failure, or letting go of your business demands strength and a positive outlook.

- Financial Planning: Ensuring your financial health is secured, regardless of the business’s outcome, is crucial. This involves prudent financial management, investment in personal and business savings, and possibly consulting with financial advisors to protect your interests.

Navigating the renewal or decline phase requires a clear assessment of your business’s current position and the external market environment. Whether you rejuvenate your business or prepare for an exit, the decisions should be strategic, well-planned, and aligned with your personal and business goals.

Understanding and effectively managing through the different stages of the business lifecycle is a testament to your resilience, adaptability, and strategic foresight as a business owner. Each stage presents unique challenges and opportunities, and how you navigate these can define the legacy of your business. Embrace each phase with a proactive, informed approach, and remember, the journey of entrepreneurship is a marathon, not a sprint. Success lies in continuous learning, evolving, and adapting to the ever-changing business landscape.

Managing Transitions Between Stages

You must recognize and manage the transition between stages to navigate the business lifecycle. These transitions offer opportunities for growth and reevaluation but also pose significant challenges.

Key Indicators for Stage Transitions

- Growth Metrics: A consistent growth pattern in sales, customer base, or market share might indicate it’s time to move from the startup to the growth stage.

- Market Saturation: When growth begins to plateau and the market feels saturated, it might be time to consider strategies suitable for the maturity stage.

- Innovation and Opportunity: New technologies or market trends can offer opportunities for renewal, signaling a shift from maturity or decline back into growth.

Strategies for Smooth Transitions

- Planning: Anticipate potential transitions by regularly reviewing your business plan and market position. This foresight allows you to prepare and adapt your strategies ahead of time.

- Flexibility: While planning is crucial, so is flexibility. The ability to pivot and adapt to unexpected market or business changes is valuable during transitions.

- Stakeholder Engagement: Keep open lines of communication with your employees, customers, suppliers, and investors. Their feedback can provide insights into how your business is perceived and what changes might be necessary.

- Resource Allocation: Ensure you have the resources to support a transition. This might mean securing additional funding, investing in new technologies, or reallocating personnel to growth areas.

- Continuous Learning: Stay informed about your industry and market trends. Attend workshops, conferences, and other learning opportunities. Knowledge is a powerful tool to help you anticipate changes and make informed decisions.

Each stage of the business lifecycle presents unique challenges and opportunities, and managing transitions effectively is crucial for long-term success. Be proactive, engage with stakeholders, and continuously learn so you can confidently guide your business through its phases.

Conclusion

Navigating the business lifecycle is a testament to the resilience and adaptability of business owners. Each stage presents challenges and opportunities, from the initial spark of an idea to the potential for renewal or graceful exit.

Understanding each stage’s importance and navigating transitions between them effectively is crucial for long-term success. Proactive planning and strategic decision-making are essential whether you’re in the early stages of ideation and conception, experiencing rapid growth and expansion, or facing the challenges of maturity and potential decline.

Stay focused on your goals, but remain flexible in your approach. Seek customer, employee, and stakeholder feedback and use it to refine your strategies and offerings. Never stop learning and growing as a business owner and leader.

Share with: